Can broadcasters pull together in a show of united strength?

We all know what’s happening with adspend. Digital advertising spend represents all net growth in adspend, and three big players are in control of that flow of cash. It’s an issue that isn’t going to be solved any time soon, and in the meantime the competition for the squeezed remainder is only getting fiercer.

As part of that various broadcasters, platforms and advertisers are reappraising the metrics they’ve traditionally used to demonstrate their superiority (or otherwise) compared to their competitors. In the US, for instance, the television and radio broadcast network CBS has failed to come to terms with the measurement company Nielsen, leaving the broadcaster without one of the most-cited measurements. As Variety’s Brian Steinberg explains, part of the issue is that broadcasters like CBS argue that Nielsen’s metrics fail to take into account viewing across a variety of platforms. The rise of VOD and the diffusion of television content across different devices means that – at least in theory – more people are being exposed to television content than ever before:

“TV networks have long based their advertising rates on Nielsen’s measure of linear TV audiences, which have slipped as consumers embrace Netflix, Hulu, Amazon Prime and other streaming and on-demand options. In such an environment, TV networks believe Nielsen’s overnight ratings are no longer the critical yardstick of viewership they once were.”

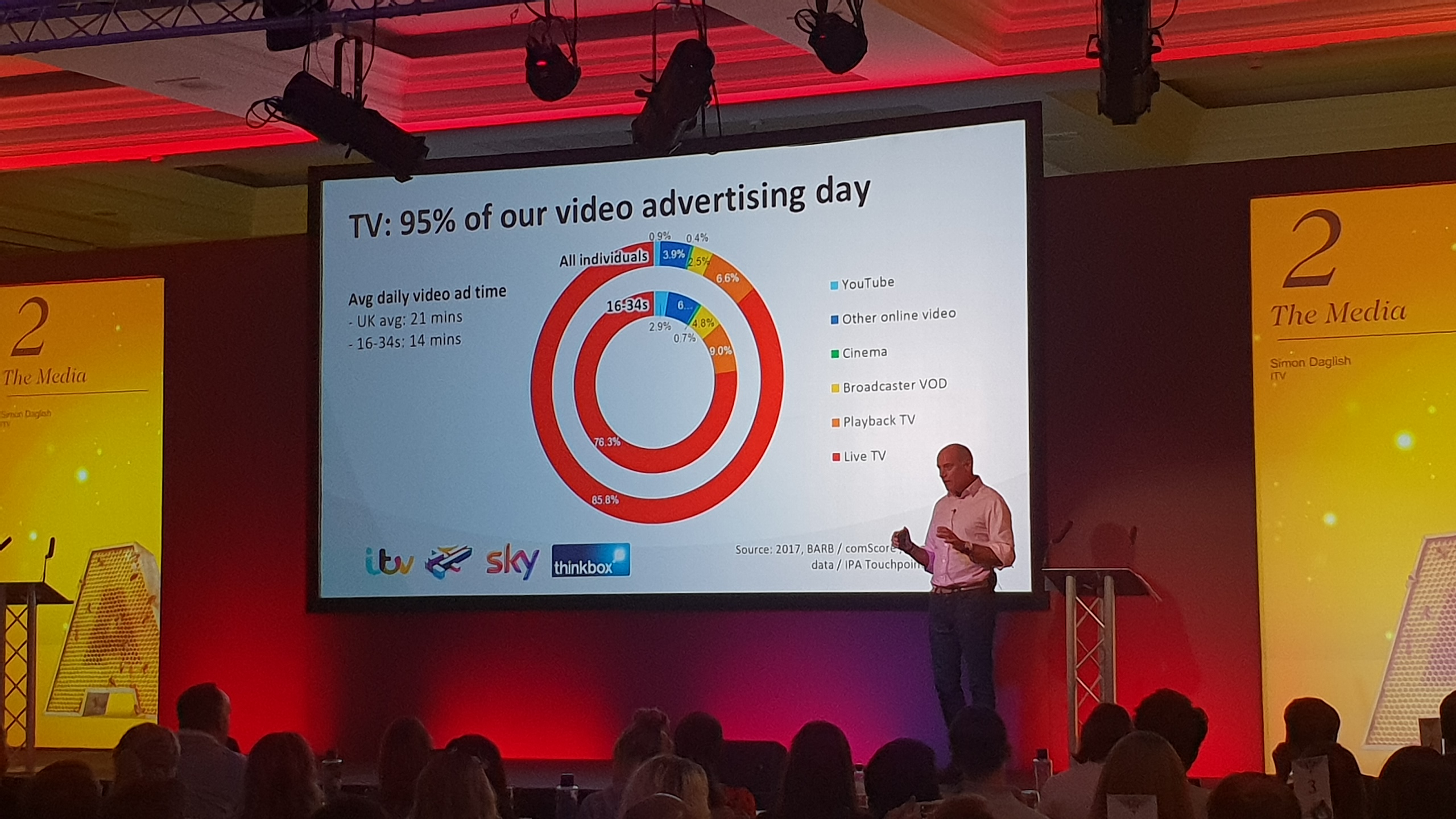

It’s a feeling that’s being expressed on the other side of the Atlantic too, with ITV’s Simon Daglish expressing the opinion that television isn’t dying, it’s “having fucking babies”. Speaking at the Media Business Course in November, he cited combined data from BARB, comScore and the IPA to back up those claims, noting that the under 34 demographic is habituated to consuming television content across more devices than ever, and with the implication that there is still room for ad growth in terms of how much time people spend with video ads on the new platforms.

{kind=link}

Despite that optimism, as Daglish’s data demonstrates, most television companies still bring in the vast majority of their ad revenue from linear viewership, and the same is true in the US. While television adspend in the UK is seeing a slight resurgence according to the latest AA/Warc and GroupM adspend figures, indications are that life isn’t going to be especially easy for television over the coming years. It makes some sense, then, for CBS to effectively start opting out of Nielsen measurements that show linear television viewership to have plateau’d and to potentially partner with comScore to demonstrate the upside to that.

(Compounding the issue slightly for CBS and its ilk is the fact that some of their biggest competitors in the video on demand space are subscription-based rather than ad-supported, and therefore don’t have the same compunction to provide verifiable viewership stats and figures. Despite that, however, there’s a credible argument to be made that the top of Netflix’s recommendations is currently the most valuable piece of media real estate in the world.)

The problem is that cross-industry measurements engender trust among potential advertisers, and that it’s currently very difficult to accurately measure audiences across platforms and devices. As the director of media at ISBA Stephen Chester has argued in The Drum, the creation of effective cross-media measurement is a must for the media industry, but it requires everyone to pull together:

“We believe one of the fundamental requirements of effective cross-media measurement is the ability to provide the same Opportunity To See (OTS) across all platforms. If you think about it, it’s only when we enter the realms of digital advertising that viewability actually becomes a conversation. 100% in-view is standard for all other forms of media and if it can be bought in print, radio or TV, advertisers want the option to buy it online if they choose.”

Whatever else happens with advertising over the course of 2019, the coalescing of traditional mediums and digital will continue. Broadcasters will need to find ways to demonstrate their cross-media appeal to potential advertisers and the industry more widely if they are to compete with the bigger players who are hoovering up the adspend growth and OTT subscription money – but in the process of doing so might find themselves undercutting the most valuable part of their business.

Chris Sutcliffe

enquiries@trippassociates.co.uk

Martin Tripp Associates is a London-based executive search consultancy. While we are best-known for our work across the media, information, technology, communications and entertainment sectors, we have also worked with some of the world’s biggest brands on challenging senior positions. Feel free to contact us to discuss any of the issues raised in this blog.